Weekly Outlook

What Happened This Week?

Eurozone

● European Central Bank meeting accounts showed several policymakers were already open to raising rates at the April meeting.

● Markets now expect the ECB to lift its key interest rate to 2.25% at the June 11 meeting due to inflation and energy-price pressures.

● The ECB kept rates unchanged at 2% in April but maintained a hawkish tone amid rising geopolitical risks.

● ECB President Christine Lagarde warned central bank independence is increasingly under pressure from governments, rising debt levels, and fragile financial systems.

● The ECB warned investors may be underestimating the financial risks linked to the Middle East conflict and elevated sovereign debt levels.

● Officials said market reactions so far appear complacent, leaving eurozone assets vulnerable to abrupt repricing.

● Rising U.S. and Japanese bond yields, combined with hedge-fund positioning, could create additional pressure on European bond markets.

● Eurozone business and consumer confidence improved slightly in May, rising to 93.5 from 93.2 in April.

● Selling-price expectations eased across business sectors but remained above historical averages.

● The European Commission lowered its 2026 eurozone growth forecast to 0.9% while increasing its inflation projection to 3.0%.

France

● French consumer confidence dropped to 82 in May from 84 previously, marking the weakest reading since March 2023.

● Households became more pessimistic about their financial situation and major purchase plans.

● Rising energy prices and uncertainty surrounding the Iran conflict continued to weigh on sentiment.

United States

● The U.S. housing market slowdown extended into a fourth consecutive year, forcing many real-estate professionals to leave the industry or seek additional income sources.

● Mortgage brokers, appraisers, photographers, and other housing-related industries also faced weaker activity.

● Home-price growth slowed further in March as higher borrowing costs weighed on demand.

● The S&P CoreLogic Case-Shiller National Home Price Index rose 0.7% year-over-year.

● Rising prices for lumber, copper, aluminum, fuel, and chemicals increased construction and renovation costs, worsening housing affordability pressures.

● Mortgage rates climbed to 6.51% amid a global bond-market selloff and persistent inflation concerns.

● The personal-consumption expenditures price index rose 0.4% in April, with annual inflation holding at 3.8%, well above the Federal Reserve’s 2% target.

● New Federal Reserve Chair Kevin Warsh faces mounting pressure as inflation remains elevated while President Donald Trump continues to favor lower interest rates.

● Chicago Fed President Austan Goolsbee warned the U.S. economy risks moving into a stagflationary environment.

● Federal Reserve Governor Lisa Cook said policymakers remain prepared to raise rates if inflation does not ease quickly enough.

● Cook noted inflation risks remain skewed to the upside despite expectations for a stable labor market.

● Manufacturing activity in the Richmond Fed region improved sharply in May, with the index rising to 13 from 3 previously.

● Businesses also reported easing price pressures and expected inflation moderation ahead.

● Consumer confidence weakened as inflation fears linked to the Middle East conflict intensified.

● The Conference Board’s consumer confidence index fell to 93.1 in May, while consumers’ assessment of business and labor-market conditions also deteriorated.

● The University of Michigan survey showed consumer sentiment fell to a record low as inflation expectations worsened.

● Initial jobless claims rose to 215,000 during the latest week, while continuing claims increased to 1.79 million.

● U.S. first-quarter GDP growth was revised down to 1.6% from 2.0%, mainly due to weaker consumer spending and lower inventory investment.

● Despite slower growth, after-tax corporate profits increased 3.3% quarter-over-quarter and 17% year-over-year.

China

● Chinese industrial firms posted a strong 24.7% increase in profits in April compared with a year earlier.

● Energy-related industries and technology manufacturing remained key growth drivers.

● Chemical-sector profits jumped 73.4%, while nonferrous metals profits surged 117.8% during the January-April period.

● Consumer-focused sectors continued to struggle due to weak domestic demand and slower economic activity.

Canada

● Canadian manufacturing shipments increased an estimated 4.6% in April, marking a third straight monthly gain.

● Petroleum and coal products led the increase as higher energy prices boosted revenues.

● The S&P Global manufacturing PMI improved to 53.3, signaling stronger industrial activity.

● Canadian banks strengthened their balance sheets and remain capable of lending even if geopolitical tensions escalate further.

● The Bank of Canada said households and businesses have remained relatively resilient despite earlier concerns over trade tensions and mortgage renewals.

● Officials nevertheless highlighted elevated risks tied to geopolitical instability and stretched valuations in equity and corporate-bond markets.

South Korea

● The Bank of Korea kept its benchmark interest rate unchanged at 2.50% but signaled that future hikes remain possible.

● Policymakers raised their 2026 economic growth forecast to 2.6%.

● The central bank also lifted its inflation outlook, forecasting headline inflation at 2.7% and core inflation at 2.4% next year.

● Consumer inflation accelerated to 2.6% in April, the highest level in 21 months, largely due to rising oil prices.

Mexico

● The Bank of Mexico lowered its 2026 growth forecast to 1.1% from 1.6% after a weak first quarter.

● Officials cited uncertainty surrounding the USMCA review and geopolitical tensions as major downside risks.

● Mexico’s central bank cut its benchmark rate to 6.5% on May 7, effectively signaling the end of its easing cycle.

Australia

● Australia’s annual inflation rate slowed to 4.2% in April from 4.6% previously.

● The moderation was mainly linked to a temporary fuel tax cut that reduced transportation costs.

● Underlying inflation pressures remained elevated, with trimmed mean inflation rising to 3.4%.

● Markets increasingly see the risk of another Reserve Bank of Australia rate increase if price pressures persist.

New Zealand

● New Zealand’s central bank held its official cash rate at 2.25% for a third consecutive meeting.

● Policymakers remained divided, with three external members voting for a 25-basis-point increase.

● Officials preferred to evaluate the economic impact of the Middle East conflict before tightening further.

● First-quarter consumer inflation accelerated to 3.1%, remaining above the central bank’s target range.

Japan

● Bank of Japan Governor Kazuo Ueda said the current energy shock could significantly alter Japan’s inflation outlook.

● Ueda noted oil-price increases affect inflation through multiple channels, including wages, demand, currency moves, and expectations.

● The BOJ policy board remains concerned about rising crude prices, increasing speculation over a possible June interest-rate hike.

This Week’s Market Movers

Forex

EUR/USD:

● The ZAR/JPY is up more than 1.9%.

● The NZD/JPY, the NZD/CAD and the NZD/CHF are up more than 1.6%.

● The NZD/USD is up more than 1.5%.

● The JPY/NZD, the CAD/NZD, the GBP/UHF and the USD/UHF are down more than 1.5%.

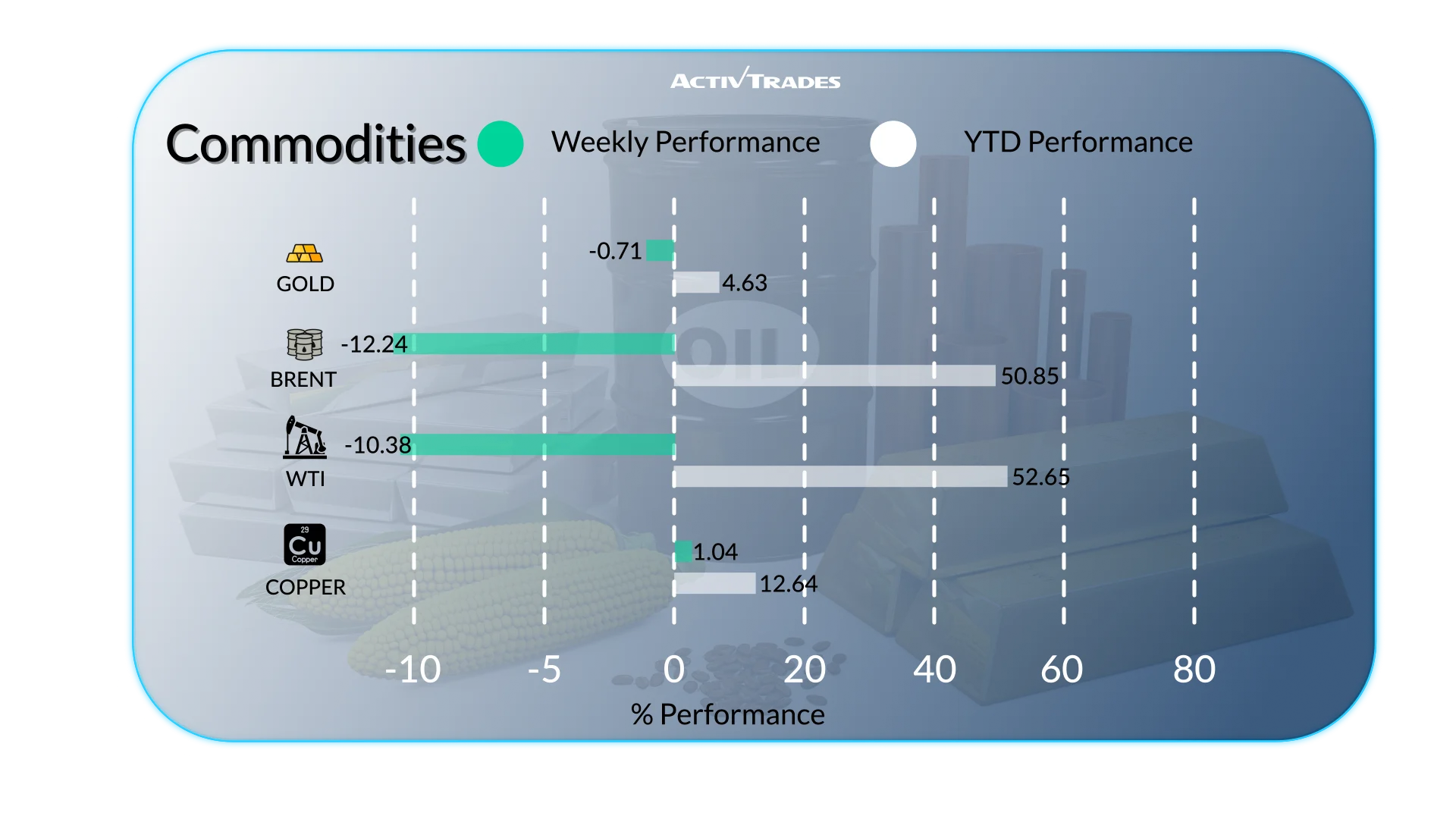

Commodities

● Natural Gas prices are up more than 9%.

● US Cocoa prices are up more than 7%.

● US Soybeans prices are up more than 3.5%.

● WTI and Brent prices are down more than 8%.

● US Sugar prices are down more than 5%.

Indices

● The Japan 225 index is up more than 10%.

● The Kospi index is up more than 7%.

● The VIX index is down more than 10%.

● The Bist 100 index is down more than 2%.

Shares

Tops

● Dell Technologies: +30.49%

● First Solar: +27.90%

● Ford Motor: +26.42%

● ARM: +25.62%

● Micron Technology: +25.42%

● AppLovin: +24.98%

● Best Buy: +24.09%

● Dollar Tree: +21.08%

● Amphemol: +20.77%

● United Airlines: +20.57%

● QUALCOMM: +19.98%

● Sandisk: +19.18%

● Advanced Micro Devices: +17.22%

● Infineon Technologies: +16.88%

● International Business Machines: +13.60%

● Zalando: +12.82%

● JD Sports Fashion: +12.50%

Flops

● Zscaler: -24.07%

● PDD Holdings: -14.02%

● Boston Scientific: -12.35%

● AutoZone: -11.52%

● Autotrader: -10.89%

Important Events to Follow

Monday 01 June

● 01:45 AM - Chinese - RatingDog Manufacturing PMI (May)

○ Previous: 52.2

○ Forecast: 51.9

● 07:15 AM - Spanish - S&P Global Manufacturing PMI (May)

○ Previous: 51.7

○ Forecast: 51.2

● 07:30 AM - Swiss - procure.ch Manufacturing PMI (May)

○ Previous: 54.5

○ Forecast: 53.8

● 07:50 AM - French - S&P Global Manufacturing PMI Final (May)

○ Previous: 52.8

○ Forecast: 48.9

● 07:55 AM - German - S&P Global Manufacturing PMI Final (May)

○ Previous: 51.4

○ Forecast: 49.9

● 08:00 AM - European - S&P Global Manufacturing PMI Final (May)

○ Previous: 52.2

○ Forecast: 51.4

● 08:30 AM - UK - S&P Global Manufacturing PMI Final (May)

○ Previous: 53.7

○ Forecast: 53.7

● 01:30 PM - Canadian - S&P Global Manufacturing PMI (May)

○ Previous: 53.3

○ Forecast: 52

● 01:45 PM - American - S&P Global Manufacturing PMI Final (May)

○ Previous: 54.5

○ Forecast: 55.3

● 02:00 PM - American - ISM Manufacturing PMI (May)

○ Previous: 52.7

○ Forecast: 52.6

Tuesday 02 June

● 09:00 AM - European - Inflation Rate YoY Flash (May)

○ Previous: 3%

○ Forecast: 3.4%

● 02:00 PM - American - JOLTs Job Openings (April)

○ Previous: 6.866M

○ Forecast: 6.8M

● 11:00 PM - Australian - S&P Global Composite PMI Final (May)

○ Previous: 50.4

○ Forecast: 47.8

● 11:00 PM - Australian - S&P Global Services PMI Final (May)

○ Previous: 50.7

○ Forecast: 47.7

Wednesday 03 June

● 01:30 AM - Australian - GDP Growth Rate QoQ (Q1)

○ Previous: 0.8%

○ Forecast: 0.5%

● 01:45 AM - Chinese - RatingDog Services PMI (May)

○ Previous: 52.6

○ Forecast: 52.5

● 01:45 AM - Chinese - RatingDog Composite PMI (May)

○ Previous: 53.1

○ Forecast: 52.8

● 07:15 AM - Spanish - S&P Global Services PMI (May)

○ Previous: 47.9

○ Forecast: 55.8

● 07:15 AM - Spanish - S&P Global Composite PMI (May)

○ Previous: 48.7

○ Forecast: 54.6

● 07:50 AM - French - S&P Global Composite PMI Final (May)

○ Previous: 47.6

○ Forecast: 43.5

● 07:50 AM - French - S&P Global Services PMI Final (May)

○ Previous: 46.5

○ Forecast: 42.9

● 07:55 AM - German - S&P Global Composite PMI Final (May)

○ Previous: 48.4

○ Forecast: 48.6

● 07:55 AM - German - S&P Global Services PMI Final (May)

○ Previous: 46.9

○ Forecast: 47.8

● 08:00 AM - European - S&P Global Composite PMI Final (May)

○ Previous: 48.8

○ Forecast: 47.5

● 08:00 AM - European - S&P Global Services PMI Final (May)

○ Previous: 47.6

○ Forecast: 46.4

● 08:30 AM - UK - S&P Global Composite PMI Final (May)

○ Previous: 52.6

○ Forecast: 48.5

● 08:30 AM - UK - S&P Global Services PMI Final (May)

○ Previous: 52.7

○ Forecast: 47.9

● 01:30 PM - Canadian - S&P Global Composite PMI (May)

○ Previous: 49.9

○ Forecast: 49.8

● 01:30 PM - Canadian - S&P Global Services PMI (May)

○ Previous: 49.2

○ Forecast: 49.6

● 01:45 PM - American - S&P Global Composite PMI (May)

○ Previous: 51.7

○ Forecast: 51.7

● 01:45 PM - American - S&P Global Services PMI (May)

○ Previous: 51.0

○ Forecast: 50.9

● 02:00 PM - American - ISM Services PMI (May)

○ Previous: 53.6

○ Forecast: 53.6

Thursday 04 June

● 01:30 AM - Australian - Balance of Trade (April)

○ Previous: A$-1.841B

○ Forecast: A$-3.0B

● 07:30 AM - European - S&P Global Construction PMI (May)

○ Previous: 41.7

○ Forecast: 41.5

● 07:30 AM - French - S&P Global Construction PMI (May)

○ Previous: 38.1

○ Forecast: 38

● 07:30 AM - German - S&P Global Construction PMI (May)

○ Previous: 42.1

○ Forecast: 42

● 08:30 AM - UK - S&P Global Construction PMI (May)

○ Previous: 39.7

○ Forecast: 40.3

Friday 05 June

● 12:30 PM - Canadian - Unemployment Rate (May)

○ Previous: 6.9%

○ Forecast: 6.9%

● 12:30 PM - American - Non Farm Payrolls (May)

○ Previous: 115K

○ Forecast: 96K

● 12:30 PM - American - Unemployment Rate (May)

○ Previous: 4.3%

○ Forecast: 4.3%

● 02:00 PM - Canadian - Ivey PMI s.a (May)

○ Previous: 57.7

○ Forecast: 51

Major Earnings Reports to Watch

Monday 01 June

● Hewlett Packard

Tuesday 02 June

● Dollar General

Wednesday 03 June

● Medtronic

● Broadcom

● Industria de Diseno Textil

Source: The Wall Street Journal, Investing, Trading Economics, Reuters, TradingView and ActivTrades’ Data as of May 29, 2026

The information provided does not constitute investment research. The material has not been prepared in accordance with the legal requirements designed to promote the independence of investment research and as such is to be considered to be a marketing communication.

All information has been prepared by ActivTrades (“AT”). The information does not contain a record of AT’s prices, or an offer of or solicitation for a transaction in any financial instrument. No representation or warranty is given as to the accuracy or completeness of this information.

Any material provided does not have regard to the specific investment objective and financial situation of any person who may receive it. Past performance is not a reliable indicator of future performance. AT provides an execution-only service. Consequently, any person acting on the information provided does so at their own risk. Forecasts are not guarantees. Rates may change. Political risk is unpredictable. Central bank actions may vary. Platforms’ tools do not guarantee success.